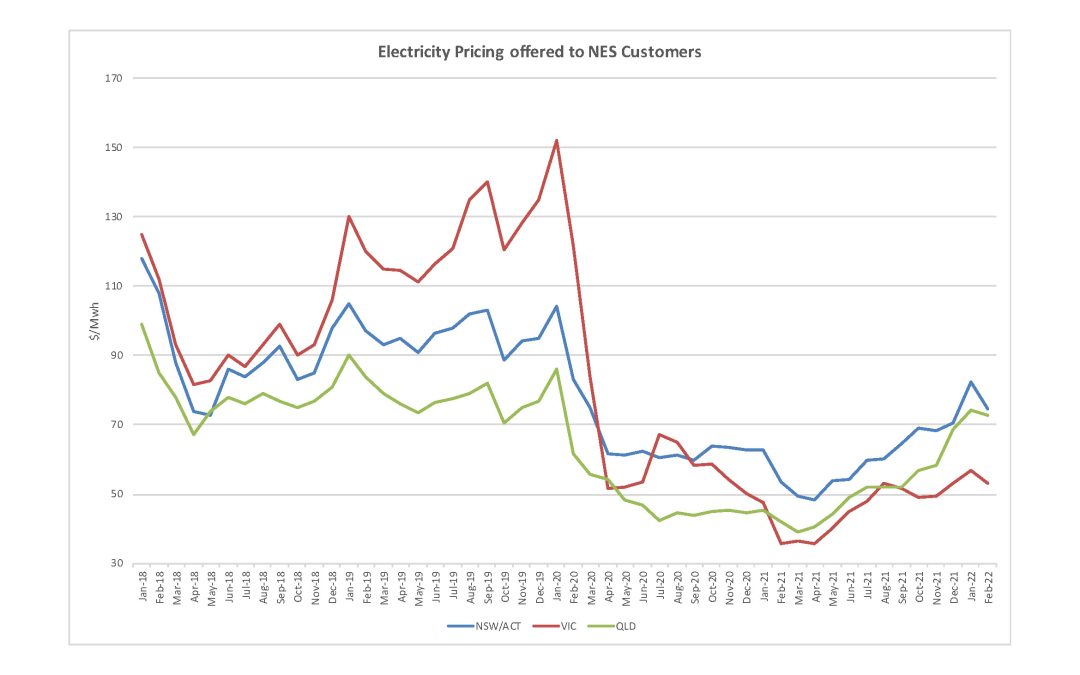

Since the withdrawal of the Hazelwood Power Station in Victoria in 2017, pricing was extremely volatile with new contracts are predominantly delivering a decrease in energy costs to existing contracts from 2021 to 2023. Significant impacts to demand during COVID shutdowns accelerated the decrease in energy pricing significantly during 2020 and 2021, as global markets started to reopen, Coal and Gas pricing increased globally which has further influenced increases in price. Pricing for premium Australian thermal coal reached records highs during Q4 2021 and is expected to be sustained at current levels.

Network tariffs continue to remain stable with the significant increases of prior years no longer prevailing, there remains however a continuing trend continuing towards increases in Demand and Capacity charges and kVa based tariffs, we are also seeing increasing prevalence of “Summer” Demand penalties during peak demand periods, this is increasing the incentive for customers to reduce demand which reduces the requirement for investment in new infrastructure.

Spot market pricing decreased significantly during 2021 but has increased during late 2021 and into 2022.

With recent announcements of Coal Generator closures coming forward at Eraring and Liddell, there has commenced a sense of panic in the market and pricing has started to increase, despite the material new renewable generation coming online and reduced demand forecast. Developments in sanctions of Russian Gas supply is expected to see domestic gas pricing increase as it is largely influenced by the global market, this will flow through to increased cost of generation for gas-fired generators.

#energysavings #renewableenergy #negawattenergy #demandresponse #energyefficiency