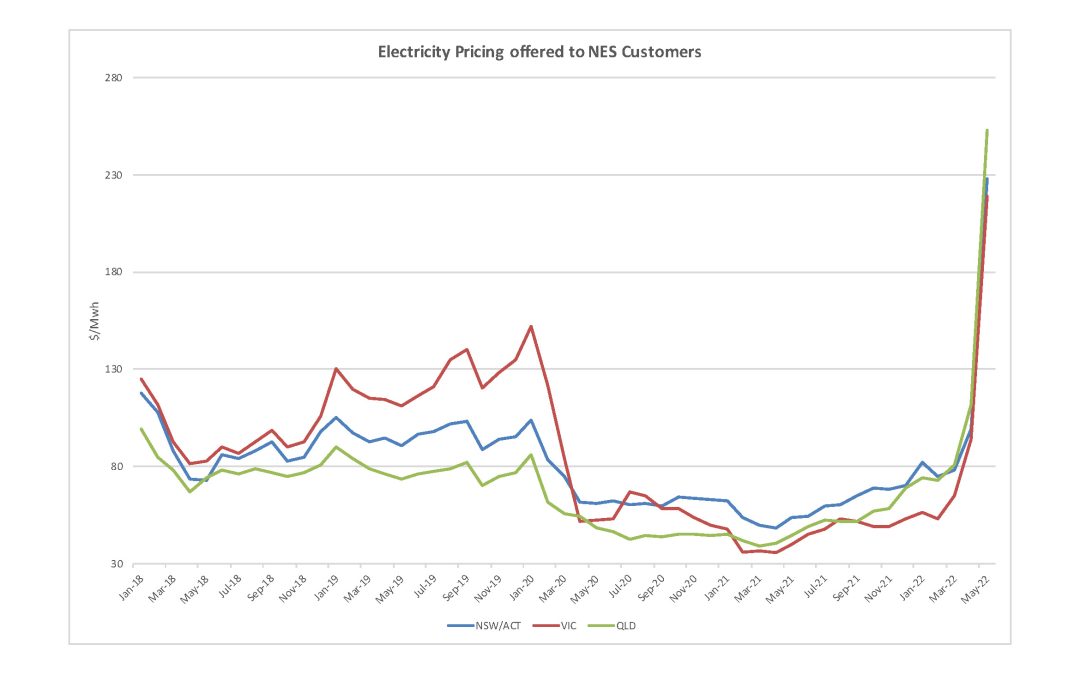

Anyone sitting on a contract renewed during 2020 or 2021, or forward contracted for July 2022 start, should be pretty pleased you are an NES customer right now and avoiding the pricing explosion that has occurred. But be warned, it is highly probable you will receive some pricing shock when those contracts come due for renewal in the next couple of years. Whilst pricing during 2020 and 2021 had decreased significantly, recent events has seen pricing reach unprecedented highs. A combination of events has caused this, with some softening expected in coming months and more material reductions forecast for 2023 and beyond.

The main causes of these pricing shocks are:

- Generation Asset Failures – A number of generation assets have failed, roughly 30% of the NEM capacity has been offline due to these failures, this alone would normally lead to a significant increase in costs. Some of these assets are soon to be recommissioned, with others coming back online over the next few months.

- Global Gas and Coal Prices – Global gas and coal demand has increased significantly due to sanctions affecting gas and coal imports into Europe, these international pricing surges flow through to domestic pricing, which is a direct pass through pricing impact to electricity generation. Domestic Spot pricing for Gas has quadrupled and demand for gas generation increased by 34%. Domestic Spot pricing for electricity has hit near $1,000 MWh, roughly 80 times the norm.

- Extended adverse weather conditions – Extended wet weather over recent months has materially reduced generation from Wind and Solar generation assets, both of which have been the prevalent source of new generation assets in recent years. Solar generation was down 37% in May. Higher levels of moisture in coal has impacted the efficiency of coal fired generators, requiring more coal to be used, and flood impacts have affected the supply of coal.

- Extreme cold conditions – Recent cold weather conditions have caused an increase in demand for heating, and surged this demand earlier than normal for the winter peak.

Whilst some of these impacts can be resolved over coming months, which is forecast to see pricing improve, the impact of international pricing is likely to be a longer term impact. Recent announcements by the Federal Government to review generation capacity payments and review gas reserves to be held by AEMO will further stabilize the market.

Recently, AEMO announced increases in the Default Market Offer (aka regulated price) for bundled residential and commercial tariffs for small business. From 1 July, these prices will increase, by an average of 18.3% in some areas. We strongly recommend moving to Fixed Price Plans, which do not yet reflect recent increases in wholesale costs, with retailers in advance of these increases.

#energysavings #renewableenergy #negawattenergy #demandresponse #energyefficiency